fjrigjwwe9r3SDArtiMast:ArtiCont

Financial rules are generic in nature and may not apply in all conditions. Take the rules and adapt them to your particular situation to get the best out of your money

There are rules prescribed to help you save, invest and reach your financial goals. But even the most diligent find it difficult to always live by the rules. More often than not this is because there isn’t any one-size-fits-all solution to financial problems. Here is a list of rules that you could rewrite when warranted. Doing so may actually help rather than hinder you on your financial path.

Pay off debt

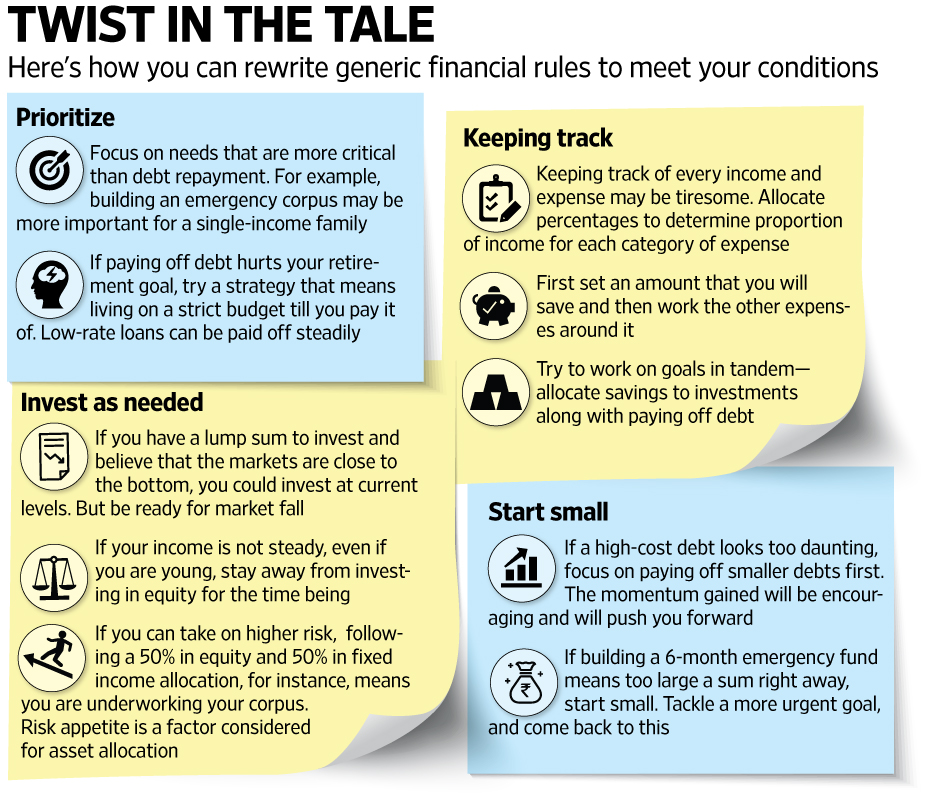

Debt versus investments: Sometimes a singular focus on debt to the exclusion of all other financial needs may do you more harm than good. A better route would be to assess your specific financial situation and prioritize. For example, if you are a single-income family then an emergency fund is a primary protection need. If you are self-employed, then saving for retirement is very important. Build a plan that allows you to allocate savings to your investment priorities along with paying off debt. If possible, find more savings and consider a second income.

High-cost debt: When a large portion of the outstanding debt is in high-cost debt, say, a credit card balance, it can take a long time to wipe it off the books, and the amount may seem daunting. This can be a downer for people who are motivated by seeing results. For such people, a more sustainable debt-reduction plan would be one where the smaller debt, in terms of value, is tackled first. As each item of debt is crossed off the outstanding list, the momentum to stay the course and pay off the rest builds up leading to a greater chance of success.

Debt-free retirement: If you draw on your retirement corpus to pay off debt, you may be compromising the income you will have in retirement. Instead, have a plan that includes living on a strict budget till you pay it off. You could also find a job in retirement that will help service the debt. If the debt has a fixed low rate of interest, then it becomes easier to service. Similarly, debt that has tax benefits such as home loans and student loans have lower effective costs.

Invest in instalments

In a rising market, investing in tranches leads to higher cost of acquisition. If you are investing through a route like a systematic investment plan (SIP), this high cost may get off set when markets are down. But what if you invest in lump sum? If you have a lump sum to invest and believe that the markets are close to the bottom, then it may make sense to invest at current levels. But make that decision only if you are willing to take the risk of a possible fall in prices after you have invested before they start rising again.

Income, expense details

If the time and effort involved in listing and tracking every item of expense is what is keeping you away from a budget and a more disciplined approach to income and expenses, then it may be worth looking for another way. One such approach would be to use percentages instead of absolute numbers to determine what proportion of the income would be allocated to each category of expense. Use your own experience to determine the percentage allocations to different broad heads of expenses such as housing, food, transportation and the like. But do remember to make the first allocation to savings and then work the other expenses around it. .

6-month emergency fund

The trade-off for the security a 6-month emergency fund gives you is that a large sum of money will be invested in such a way that it earns a much lower return than what it otherwise could since the emergency fund is typically held in low-risk liquid investments. Plus, if building this corpus is your immediate priority, in the time that it takes you to build this 6-month corpus, your other goals are ignored. If the total amount or the time frame seems daunting, aim for a smaller number. After some time, or after having tackled a more urgent goal, you can come back to the emergency corpus and make it bigger. Also, in some circumstances, a smaller emergency fund may suffice. For example, if it’s a household with two comparable regular incomes, high job security and a low level of debt. If you qualify, then it frees up your saving to catch up on other goals.

Asset allocation rules

Broad asset allocation rules prescribed do not apply to specific situations. For example, one rule is that 100 or 120 minus your age is the percentage of equity exposure that your portfolio should have. This also gives a younger investor greater exposure to equity. But if your income has not stabilized then growth investments like equity may not be suitable. Or, if you follow a 50% in equity and 50% in fixed income allocation, it may mean that you are underworking your corpus when you are in the situation to take higher risks for better returns.

Financial rules are tried and tested approaches to managing money. Recast them to your particular situation so that you are able to take the best decisions for your finances.